The basics of ESOS – qualification criteria, timelines, compliance routes and tools. What are the advantages and disadvantages? What are the exceptions and the loopholes in the framework?

New year, new regs! There were two reasons to celebrate (or commiserate) on the 31st of December – not only was it the last day of 2014 but also the qualification date for phase 1 of ESOS. Over the next few paragraphs we will take you through the key bits of what ESOS is about and discuss the merits (and flaws?) of the regulatory framework.

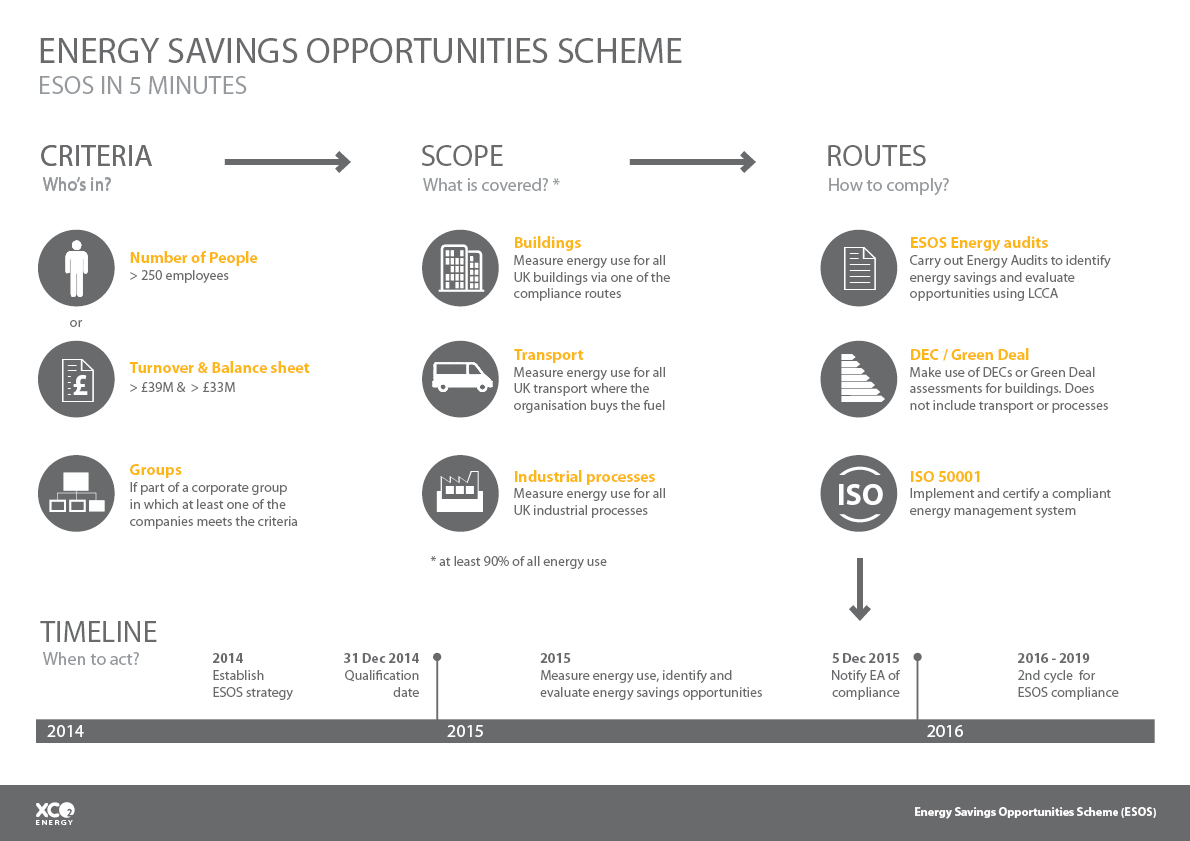

The Energy Savings Opportunity Scheme (ESOS), launched in June 2014, represents the UK’s response to the Article 8 – Energy Audits – of the EU Energy Efficiency Directive. Run by the Environmental Agency, it is a mandatory energy assessment scheme aimed at large organisations, which establishes the obligation to audit energy use and identify energy saving opportunities.

Criteria Organisations with either more than 250 employees, or an annual turnover in excess of £39M (€50M), and a balance sheet in excess of £33M (€43M), are considered large undertakings and, therefore, must comply with ESOS. Corporate groups in which one of the companies based in the UK fulfils the criteria also need to comply. The qualification criteria are set to include 7,500 – 10,000 large organisations. SMEs are left out of the scheme and so are public sector organisations.

Scope ESOS requires organisations to measure at least 90% of their energy consumption from buildings, transport and industrial processes. A flexible approach is encouraged, meaning that specific energy uses or buildings representing less than 10% in total can be left out and that data for similar buildings can be extrapolated, allowing for a degree of sampling.

Routes There are alternative routes to ESOS compliance: Energy audits, representative of the portfolio; Display Energy Certificates or Green Deal assessments, for all buildings; and ISO 50001 implementation and certification. It should be noted that these routes naturally have pros and cons, and are particularly suited for specific cases. This will be the subject of a follow up post.

Compliance In order to achieve compliance, organisations need to track at least 12 months’ worth of energy data (which must overlap with the qualification date), identify energy efficiency measures and evaluate their potential cost and savings using life cycle cost analysis. In this process, it is a requirement to engage with an accredited Lead Assessor, which will carry out and/or oversee the work and compile an evidence pack. There is also a requirement for board buy in, via director’s sign off.

Timelines The scheme runs in 4 years compliance cycles. For the first cycle, participants need to inform the Environmental Agency of compliance via an online submission by 5th December 2015.

Advantages/disadvantages The Government is taking a light touch approach to implementing this regulation. The scheme is designed to be flexible, allowing businesses to choose the most appropriate route and to re-use existing data and reports. The requirement for board buy-in is quite positive, as often energy savings initiatives tend to be pushed to the bottom of corporate agendas. However, lifecycle cost analysis is mandated where it is reasonable to carry out. The implementation of the energy saving opportunities identified is not compulsory. Additionally, energy data that could aid benchmarking will not be gathered as part of the scheme.

Exceptions/loopholes There are some exceptions in the regulation that may contribute to shrinking its reach. One has to do with corporate groups as these are only included if one of its parts fulfils the criteria. Hence groups split into multiple subsidiaries may escape under the radar. Equally, franchises, for instance, do not need to comply. Another significant exception is the landlord and tenant rule, akin to what happens with the Carbon Reduction Commitment (CRC), meaning that unconsumed supplies (any energy supply that is not consumed but instead provided to a third party.) are out of the equation. A significant number of offices are in this situation.

ESOS has created a buzz in the industry since it was officially launched. It generated significant interest but also many concerns that it may fail to deliver what policy makers are expecting.

The framework has the potential to set companies in the right direction for harnessing great energy and cost savings, way beyond the cost of compliance. Understanding the scheme, overcoming its limitations, and implementing the right approach will be vital in realising its potential.

Next Week our second post in this series “First steps with ESOS, 11 months and counting” will help you through the first steps prior to engaging an assessor. Considering the role of the Lead Assessor, how the chosen route influences cost and looking at how ESOS can be delivered in such a way that businesses go beyond compliance.